- Nvidia achieved a striking 114% revenue growth, reaching $130.5 billion in fiscal 2025, with EPS soaring 147% to $2.94, yet faced a 14% stock dip post-earnings.

- Macroeconomic challenges, including geopolitical tensions and upcoming U.S. AI export restrictions to China, threaten Nvidia’s market presence.

- Additional hurdles include potential U.S. tariffs on imports, impacting manufacturing costs and supply chains.

- Nvidia remains a leader in AI, leveraging its advanced Blackwell architecture and GB200 Superchips to drive innovation and efficiency.

- The AI inferencing market, projected to grow from $106 billion in 2025 to $255 billion by 2030, offers significant growth potential.

- Nvidia’s ventures into autonomous vehicles, robots, and AI systems suggest continued dominance as AI demand increases.

- Investors are encouraged to consider dollar-cost averaging amid market volatility, with Nvidia’s history of resilience offering potential growth opportunities.

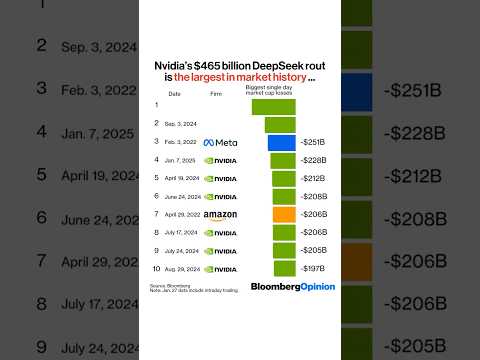

Few companies have redefined technologies as profoundly as Nvidia. In its fiscal 2025, closing on January 26, Nvidia notched a staggering 114% climb in revenue, reaching $130.5 billion, with earnings per share skyrocketing by 147% to $2.94. Yet, even these mighty figures could not shield its stock from a 14% dip post-earnings release. This downturn leaves investors pondering: Is it time to buy the dip or steer clear of the volatility ahead?

The macroeconomic landscape is rife with uncertainties, which loom large over Nvidia’s ambitious trajectory. Rising geopolitical tensions coupled with the Biden administration’s forthcoming AI export restrictions to China—set to kick in May 2025—pose formidable hurdles. Nvidia’s sales to China are already halved due to earlier export controls, and tightening these further could hobble the tech giant’s market presence there.

Adding to the complexity, potential tariffs from the U.S. administration on imports from China, Canada, and Mexico could inflate manufacturing costs and tangle supply chains. Such hurdles, combined with a slowdown in its once-booming data center segment—dropping to a mere 20% growth in Q4 of fiscal 2025—cast shadows on its premium valuation sustainability.

Yet, against this backdrop, Nvidia remains a powerful force in AI innovation, largely thanks to its trailblazing Blackwell architecture. This system, having achieved the swiftest product ramp-up in Nvidia’s history, brought in $11 billion in revenue in Q4 alone. Nvidia’s strategic focus on the burgeoning AI inferencing market, projected to grow dramatically from $106 billion in 2025 to $255 billion by 2030, could indeed steer it toward sustained dominance.

With its GB200 Superchips designed for complex computing demands of reasoning AI—requiring massively more compute power—Nvidia is poised not only to compete but to excel, offering much-needed resources at a more economical cost compared to its predecessors.

The future beckons, with Nvidia venturing into multiple AI-powered territories: the realm of autonomous vehicles to physical AI robots and agentic AI systems. Leveraging the Jevons paradox, Nvidia is set to thrive as AI becomes more efficient and widespread, thereby amplifying the demand for robust AI infrastructure.

While Nvidia’s stock has weathered more than its share of storms, historic recoveries—whether from the 2018 crypto-linked crash or the pandemic-induced plunge—demonstrate resilience. These rebounds are testament to Nvidia’s strategic pivots and robust fundamentals, suggesting yet another potential rally awaits.

Still, the path ahead requires vigilance. The tech landscape is ever-evolving; investors would do well to look beyond short-lived volatility. A strategy of dollar-cost averaging may allow investors to build a position in Nvidia while mitigating risk, embracing the opportunity of a volatile market with the wisdom of tempered optimism. The crossroads at which Nvidia stands today could be the gateway to its next exhilarating chapter in AI mastery.

Nvidia’s AI Future: Is It Worth the Investment?

Overview

Nvidia’s recent financial performance underscores its pivotal role in shaping the technology landscape. Yet, with a 14% stock decline post-earnings report, investors are left questioning the balance between opportunity and risk. As we unpack Nvidia’s current challenges and potential pathways, we aim to deliver actionable insights and help you make an informed investment decision.

How-To: Navigating Nvidia’s Investment Landscape

1. Understand Macroeconomic Risks:

– Geopolitical Tensions: Upcoming AI export restrictions to China and potential tariffs can significantly impact Nvidia. Assess playbacks like diversifying supply chains and customer bases outside geopolitical hotspots.

– Inflation and Supply Chain: Be aware of how increased manufacturing costs could compress margins.

2. Capitalize on AI Growth:

– AI Inferencing Market: Embrace Nvidia’s focus on AI inferencing, which is projected to grow from $106 billion in 2025 to $255 billion by 2030.

– Tech Innovations: Consider Nvidia’s cutting-edge Blackwell architecture and GB200 Superchips that boost AI efficiency and reduce costs.

3. Investment Strategies:

– Dollar-Cost Averaging: Minimize risk by gradually investing fixed amounts at regular intervals.

– Long-Term Horizon: Given Nvidia’s history of resilience, a long-term investment approach could capitalize on potential rebounds following temporary market volatility.

Real-World Use Cases and Industry Trends

– Autonomous Vehicles and Robotics: Nvidia’s advancements in AI support autonomous vehicles and physical AI robots, paving the way for future technological disruption.

– Agentic AI Systems: As AI systems become more sophisticated, Nvidia’s technologies are crucial for scaling future AI applications.

Limitations and Controversies

– Regulatory Barriers: Stricter AI export controls to China could significantly reduce revenue from a major market.

– Market Dependency: Heavy reliance on U.S. tech regulations and geopolitical landscapes can affect Nvidia’s sales and operations.

Insights and Predictions

– AI Infrastructure Demand: Increased AI efficiency is likely to create a surge in demand for robust AI infrastructure, benefiting Nvidia’s market positioning.

– Strategic Partnerships: Expanding partnerships across diverse industries could buffer against market-specific downturns.

Security and Sustainability

– Sustainable Practices: Nvidia is investing in energy-efficient technology to mitigate environmental impacts while enhancing computing power.

Quick Tips and Recommendations

– Stay Informed: Regularly update your knowledge of geopolitical events that could affect Nvidia.

– Diversify Portfolio: Reduce risk by including other technology sector stocks.

– Monitor Earnings: Keep an eye on Nvidia’s financial performance indicators like revenue growth and profit margins.

For more insights, visit the official link name website for comprehensive information on industry trends and technological advancements.

In conclusion, while Nvidia faces short-term challenges, its strategic focus on AI innovation and historic resilience suggest it could outperform in the long run. For investors willing to take a calculated risk, Nvidia remains a compelling option.